As the year draws to a close, we would like to take a few minutes to reflect and to look ahead. 2024 was a challenging year for the global economy and for electronics manufacturing. Many customers reported weak demand, higher costs, and reduced profits. There was widespread uncertainty due to geopolitical conflicts, US elections, and slowdowns in many parts of the world. Although US interest rates have started to drop, it remained high for most of the year which dampened investments and large purchases. While the stock market performed well for some, many faced layoffs and a decline in buying power.

Amazingly, the electronics manufacturing market recorded an increase of approximately 5% for the year. This was driven almost entirely by explosive growth in A.I., servers/cloud computing and data centers. Companies that supply these systems enjoyed high utilization, even down to the raw materials such as low-loss FR4 and low Dk glass. Other bright spots include military aerospace, renewable energy, and wearable/smart devices. There was notable slowdown in automotive and electrical vehicles, while most commercial markets including industrial, medical, and telecom were relatively flat or slightly higher compared with 2023.

Looking towards 2025, we are optimistic and planning for growth. Customers we spoke to are forecasting an overall recovery that will start in Q2. Generative AI should continue to drive demand in semiconductors, hi-end computing, and AI-powered applications and devices. The Trump administration and GOP-lead congress favors deregulation and lower taxes which should spur economic growth and corporate investments. Component leadtimes have stabilized and most firms should be done with their destocking efforts.

For the most part, cost and leadtimes for Sunshine suppliers have been stable in 2024. Leadtimes for common cores are 1 to 2 weeks with 3-4 weeks for special materials. Suppliers that offer ultra-low loss materials have seen strong demand from the AI and Hi-Speed Computing market, and this is putting stress on capacities and leadtimes for high performance FR4 and Low-Dk glass. This trend is expected to continue in 2025, even as suppliers plan for capacity expansions.

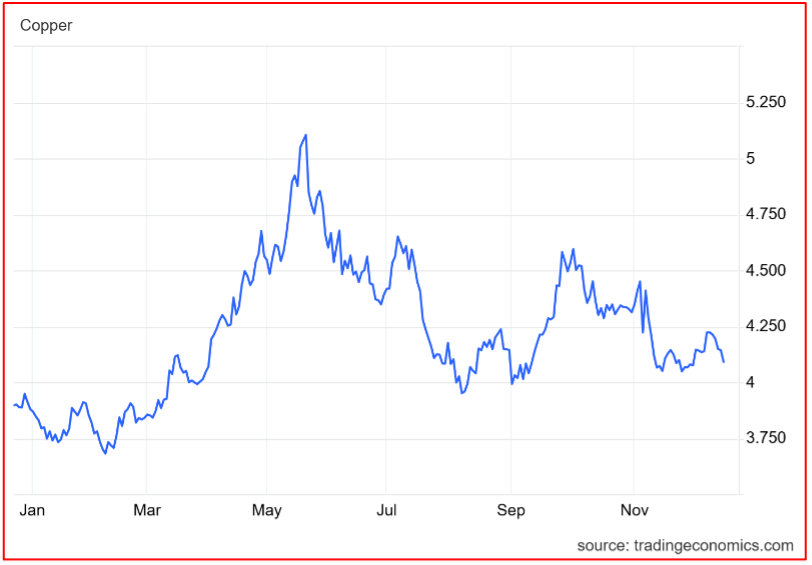

Cost of copper in Asia are on an upward trend due to higher processing cost and demand for smooth copper foils (HVLP2 and higher). Our purchasing reported copper cost was 12 RMB/kg last month, 16 RMB/kg this month, and will go up to 18 RMB/kg next month. We expect the cost of copper clad laminates to increase in 2025 but the magnitude and timing are unclear.

Market price for Copper in the past 12 months reached a peak of $5.1 USD per pound in May 2024 then it has been hovering around $4 to $4.5 in the past 6 months.